There are many options to reduce your mortgage payments. You have the option to refinance your mortgage or sublet a room or part your property. You can also get out of mortgage insurance. There are other options.

To reduce mortgage payments, you can sublease a room or part of your property.

If you do not have enough money to cover your mortgage payments and you have spare rooms, you may be able to rent them out. However, you must make sure that your sublease agreement is legal. You must also get permission from the landlord before you sublet the room.

You can reduce your mortgage payments by renting out a room or a portion of your home. However, you must be careful and screen tenants carefully because this can be a stressful experience. Before renting out a room, have prospective tenants fill out a room rental application and sign a lease agreement. You can have a contract for a set number of months, or for one month.

Removal of mortgage insurance

It is possible to reduce monthly mortgage payments by removing mortgage insurance from your loan. It will vary depending on what type of loan you have. To get rid of mortgage insurance, you must meet the LTV requirements if you take out a conventional loan. This means that you should put at least 10% down on your home. This will give you an initial loan balance $180,000.

Another option is to pay off your remaining mortgage balance and reduce your LTV. This is possible if your home has been paid off by at least 80%. However, if you have only 20% equity in your home, you may have to keep paying PMI for a longer period of time.

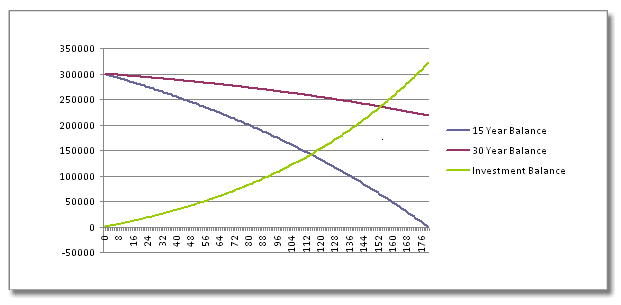

Extending your loan term

If you want to lower your monthly payments, consider extending your loan term. This will reduce your monthly payments by increasing your repayment term and decreasing the interest rate. Also, rollover delinquent payments and escrow deficits can result in lower monthly payments. However, remember that if you're going to take this option, you will have to pay PMI, which protects the lender in case of default.

You can refinance your mortgage loan to lower your monthly mortgage payments. With excellent credit you can take advantage today's low interest rates for a lower rate and lower payments. This can help save you a significant amount.

Lower rates for homeowners insurance

Finding lower rates on homeowners insurance is not always easy. You must understand the reasons behind your insurance premium. There are many things to consider. Your credit score is a major determinant of your premium. Your insurer will reduce your premium if you have good credit. If you have low credit scores, the insurance company may charge you more.

One of the most simple ways to lower your homeowners insurance is to raise the deductible. Many insurers offer lower premiums if you raise your deductible. A $1,000 deductible could save you about 12 percent each year.

FAQ

What is the average time it takes to sell my house?

It depends on many different factors, including the condition of your home, the number of similar homes currently listed for sale, the overall demand for homes in your area, the local housing market conditions, etc. It may take up to 7 days, 90 days or more depending upon these factors.

What are the downsides to a fixed-rate loan?

Fixed-rate loans have higher initial fees than adjustable-rate ones. A steep loss could also occur if you sell your home before the term ends due to the difference in the sale price and outstanding balance.

How much does it cost for windows to be replaced?

Windows replacement can be as expensive as $1,500-$3,000 each. The cost to replace all your windows depends on their size, style and brand.

What should I look out for in a mortgage broker

Mortgage brokers help people who may not be eligible for traditional mortgages. They work with a variety of lenders to find the best deal. There are some brokers that charge a fee to provide this service. Other brokers offer no-cost services.

Statistics

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

External Links

How To

How to buy a mobile home

Mobile homes can be described as houses on wheels that are towed behind one or several vehicles. They have been popular since World War II, when they were used by soldiers who had lost their homes during the war. Mobile homes are still popular among those who wish to live in a rural area. These homes are available in many sizes and styles. Some houses can be small and others large enough for multiple families. There are even some tiny ones designed just for pets!

There are two types of mobile homes. The first type is manufactured at factories where workers assemble them piece by piece. This takes place before the customer is delivered. You could also make your own mobile home. It is up to you to decide the size and whether or not it will have electricity, plumbing, or a stove. Next, make sure you have all the necessary materials to build your home. To build your new home, you will need permits.

Three things are important to remember when purchasing a mobile house. You may prefer a larger floor space as you won't always have access garage. If you are looking to move into your home quickly, you may want to choose a model that has a greater living area. You should also inspect the trailer. It could lead to problems in the future if any of the frames is damaged.

Before buying a mobile home, you should know how much you can spend. It is important to compare prices across different models and manufacturers. Also, take a look at the condition and age of the trailers. Although many dealerships offer financing options, interest rates will vary depending on the lender.

You can also rent a mobile home instead of purchasing one. You can test drive a particular model by renting it instead of buying one. Renting isn’t cheap. Renters usually pay about $300 per month.