Consider the pros and con's of a HELOC before you apply. HELOCs don't have closing fees. However, tax deductions are not available for interest charges you use to pay personal expenses. You may end up spending too much on your HELOC and tap out equity. This can lead to high principal and interest costs. The good news is that the interest rates on HELOCs are much lower than those for traditional 30-year fixed rate home equity loans.

Tax deductible interest charges on funds borrowed from a HELOC to pay personal expenses are no longer allowed

You may wonder if HELOC interest payments are still tax deductible. The good news? You still have the option to deduct up to $750,000 for interest payments on your HELOC. You can't deduct interest paid on funds you use for personal expenses like home renovations. This is because the new tax law has changed the way that you can deduct interest payments for personal expenses.

In the past homeowners were allowed to deduct up $100,000 interest from their HELOC. The new tax law limits the deduction to home improvements that increase your home's value. These improvements must not be insignificant and must increase your home's value. A substantial home improvement is any improvement that significantly improves the value of the home.

The tax code requires that any interest charges on a home equity line of credit be spent on property used as collateral. This rule also applies to personal expenses.

No closing costs to set up a HELOC

A HELOC does not have closing fees, but it is important to weigh all costs before you make a decision. The lender may charge closing costs in addition to interest rates, so you should shop around for the lowest costs before making a final decision. The average closing cost is between 2% and 5% of the total line.

HELOC is an revolving line credit that uses your equity as collateral. You can use the funds for many purposes, including home improvement and medical expenses. The equity in the home is used to determine the credit limit. The "draw period", which is usually ten years, is also used by lenders. After that, borrowers will need to start repaying the loan. The loan can be renewed if the borrower so wishes.

HELOC lenders sometimes charge closing fees. These fees are generally lower than other expenses. Depending on your lender, you may be required to pay an application and origination fee. A notary fee is also possible. These costs will help the lender ensure the loan is legally binding and is not subject to any liens. You may also be charged by the lender for a credit check or an appraisal.

A 30-year fixed rate home equity loan with lower interest rates will yield you lower interest rates

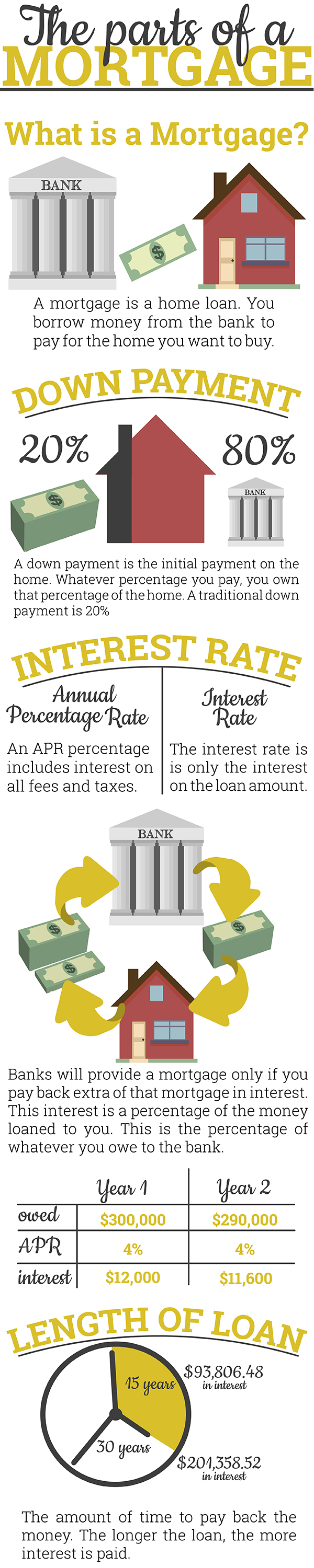

A home equity loan is a loan secured against the home's equity. The loan is paid in lump-sums and then interest-free over a predetermined period. A home equity loan of credit (HELOC), by contrast, is a creditcard that allows you to pay interest only on the amount borrowed.

A home equity loans are typically fixed-rate loans with a repayment time of five to thirty years. This means that your interest rate will remain the same regardless of what happens in the economy. A fixed-rate home equity loan usually has lower interest rates than most other loans, with some even as low at 3%.

Home equity lines of credit allow borrowers to access funds as needed. They can be used to finance a home renovation project or debt repayment. Home equity lines of credit have lower interest rates than other loans, but you will need a high credit score and a low debt-to-income ratio to qualify.

FAQ

Can I purchase a house with no down payment?

Yes! There are programs available that allow people who don't have large amounts of cash to purchase a home. These programs include government-backed loans (FHA), VA loans, USDA loans, and conventional mortgages. Visit our website for more information.

How can I tell if my house has value?

If your asking price is too low, it may be because you aren't pricing your home correctly. If your asking price is significantly below the market value, there might not be enough interest. Our free Home Value Report will provide you with information about current market conditions.

How can I repair my roof?

Roofs can become leaky due to wear and tear, weather conditions, or improper maintenance. Minor repairs and replacements can be done by roofing contractors. For more information, please contact us.

Statistics

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

External Links

How To

How to Find an Apartment

Moving to a new place is only the beginning. This process requires research and planning. It includes finding the right neighborhood, researching neighborhoods, reading reviews, and making phone calls. There are many ways to do this, but some are easier than others. Before renting an apartment, it is important to consider the following.

-

You can gather data offline as well as online to research your neighborhood. Websites such as Yelp. Zillow. Trulia.com and Realtor.com are some examples of online resources. Local newspapers, real estate agents and landlords are all offline sources.

-

Review the area where you would like to live. Yelp, TripAdvisor and Amazon provide detailed reviews of houses and apartments. Local newspaper articles can be found in the library.

-

Make phone calls to get additional information about the area and talk to people who have lived there. Ask them what the best and worst things about the area. Ask them if they have any recommendations on good places to live.

-

You should consider the rent costs in the area you are interested. If you are concerned about how much you will spend on food, you might want to rent somewhere cheaper. On the other hand, if you plan on spending a lot of money on entertainment, consider living in a more expensive location.

-

Find out about the apartment complex you'd like to move in. Is it large? What price is it? Is the facility pet-friendly? What amenities is it equipped with? Can you park near it or do you need to have parking? Are there any rules for tenants?