A mass mortgage calculator can be a helpful tool to help you compare the costs associated with renting and buying a home. There are many factors that affect the interest rate on mortgages. They fluctuate daily so your actual payment will vary. Some of these variables are beyond your control. Other factors are more easily controlled. The mass mortgage calculator can give you an estimate for your maximum monthly payment. It takes into consideration a variety factors such as down payment, purchase price and interest rate. You can also include taxes and insurance in this calculator.

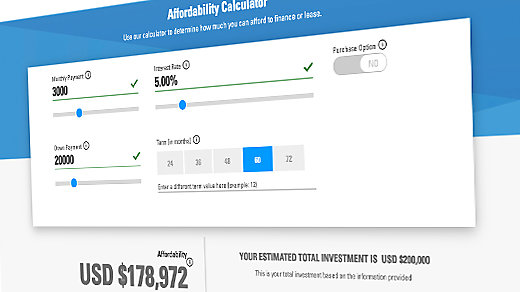

Based on the purchase price, downpayment, loan term and interest rate, this calculator estimates your maximum monthly mortgage payment.

Mass mortgage calculator uses your purchase price, down payment and home's values. This information is used by lenders to determine your maximum monthly mortgage payment. Also, include homeowners insurance and taxes. The calculator will also factor in any homeowners' association fees.

A mortgage calculator can help you compare monthly payments for different home price ranges. You can choose different loan terms depending on your financial situation and make different down payments. You can also change the interest rate which will affect your monthly payment.

Includes taxes and insurance

The Massachusetts Mortgage Calculator lets you calculate your monthly payment including insurance and PMI. It also allows you to enter additional payments such as bi-weekly payments and home owners' association fees. You can also see the amortization schedule to help you determine how long it will take to pay off your mortgage. You can export or print this information to an Excel spreadsheet, so you can examine your payment history.

The mortgage calculator allows you to estimate the amount of money you can save if additional payments are made over the life of the mortgage. Even a small additional payment can shorten your term. You can explore various mortgage scenarios to determine if they are feasible and financial wise. Before you make any final decisions, double-check all information provided by a calculator.

Does not pre-qualify you for a mortgage

Mortgage calculators estimate your monthly mortgage payment, but they do not pre-qualify you for a loan. The interest rate is dependent on many factors. Some of these are beyond your control. Calculator calculates the maximum monthly payment using information such as credit score, down payment and loan type. This calculator helps you assess your ability to pay for a house.

To use a mass loan calculator, you must input all of your income and current debt. Your total monthly income should be at least three times your current monthly debt payment, as this will give you a good idea of whether you can afford a mortgage. It is important to know how much you can pay for a downpayment.

How to adjust the default values of the mortgage calculator to reflect your current situation

A mortgage calculator will help you estimate how much you would pay each month for a home. These inputs can be used as estimates, and should always be adjusted to suit your individual circumstances. There are many organizations that offer mortgage calculators, such as Quadrant Information Services, The Tax Foundation, CoreLogic and CoreLogic. These resources can give you a good idea of your monthly payment and help you budget your finances.

The loan term and interest rate determine the default values of a mortgage calculator. The interest rate you choose should be in line with your budget and mortgage term. For example, if you are looking for a 15 years-term mortgage, you would enter the average 15 year interest rate. This default value can be adjusted to enable you to compare loans terms and get a good balance.

FAQ

Can I buy a house without having a down payment?

Yes! Yes. There are programs that will allow those with small cash reserves to purchase a home. These programs include government-backed loans (FHA), VA loans, USDA loans, and conventional mortgages. More information is available on our website.

How do I calculate my interest rate?

Interest rates change daily based on market conditions. In the last week, the average interest rate was 4.39%. Divide the length of your loan by the interest rates to calculate your interest rate. If you finance $200,000 for 20 years at 5% annually, your interest rate would be 0.05 x 20 1.1%. This equals ten basis point.

What amount of money can I get for my house?

This varies greatly based on several factors, such as the condition of your home and the amount of time it has been on the market. Zillow.com shows that the average home sells for $203,000 in the US. This

How can I tell if my house has value?

You may have an asking price too low because your home was not priced correctly. If your asking price is significantly below the market value, there might not be enough interest. To learn more about current market conditions, you can download our free Home Value Report.

Do I require flood insurance?

Flood Insurance protects from flood-related damage. Flood insurance helps protect your belongings, and your mortgage payments. Learn more information about flood insurance.

What are the three most important things to consider when purchasing a house

The three most important things when buying any kind of home are size, price, or location. Location refers the area you desire to live. Price refers the amount that you are willing and able to pay for the property. Size refers to how much space you need.

What are the pros and cons of a fixed-rate loan?

Fixed-rate mortgages lock you in to the same interest rate for the entire term of your loan. This means that you won't have to worry about rising rates. Fixed-rate loans have lower monthly payments, because they are locked in for a specific term.

Statistics

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

External Links

How To

How to Buy a Mobile Home

Mobile homes are houses constructed on wheels and towed behind a vehicle. They have been popular since World War II, when they were used by soldiers who had lost their homes during the war. People today also choose to live outside the city with mobile homes. Mobile homes come in many styles and sizes. Some houses have small footprints, while others can house multiple families. Some are made for pets only!

There are two types of mobile homes. The first type is produced in factories and assembled by workers piece by piece. This happens before the product can be delivered to the customer. The other option is to construct your own mobile home. The first thing you need to do is decide on the size of your mobile home and whether or not it should have plumbing, electricity, or a kitchen stove. Then, you'll need to ensure that you have all the materials needed to construct the house. To build your new home, you will need permits.

Three things are important to remember when purchasing a mobile house. First, you may want to choose a model that has a higher floor space because you won't always have access to a garage. A larger living space is a good option if you plan to move in to your home immediately. You'll also want to inspect the trailer. It could lead to problems in the future if any of the frames is damaged.

It is important to know your budget before buying a mobile house. It is important to compare prices across different models and manufacturers. Also, look at the condition of the trailers themselves. Many dealerships offer financing options but remember that interest rates vary greatly depending on the lender.

An alternative to buying a mobile residence is renting one. Renting allows for you to test drive the model without having to commit. Renting is not cheap. Renters usually pay about $300 per month.