Understanding the basics of a mortgage is essential before you can apply. This includes the interest rate, downpayment, assessment by the lender, and your personal information. It is important to choose the right mortgage for your home purchase. It can make an enormous difference in your quality life and your finances.

Interest rate

The interest rate on a mortgage refers to a percentage of total loan amount. The borrower pays this amount on top of the agreed loan repayments. To be able make monthly payments, it is essential to select the best mortgage interest rate. The mortgage interest rate can go up or down, so it is crucial to be on the lookout for changes.

Other costs, such as discount points or loan origination fee, are not included with the interest rate. Mortgage insurance and closing costs are also included. Borrowers will be able to see the total cost of borrowing by using the APR.

Down payment

The down payment on a mortgage is a percentage of the total value of the home that the borrower pays up front. It is typically between ten percent and fifty percent. The interest rate charged for a mortgage will be determined by how much a borrower pays down. The interest rate will usually be lower if there is a large down payment. A large downpayment lowers the risk for banks when they lend mortgages.

While there are no hard and fast rules as to how much down payment you need, there are some factors you should consider when determining your down payment. A low downpayment is risky. Therefore, it's better if you can afford at least fifty percent. Borrowers who are able to put up at least fifty percent to sixty percent of the purchase cost will be more likely to get money from a bank. Banks will typically refuse to lend money if the down payment you make is not sufficient or you don’t have enough savings.

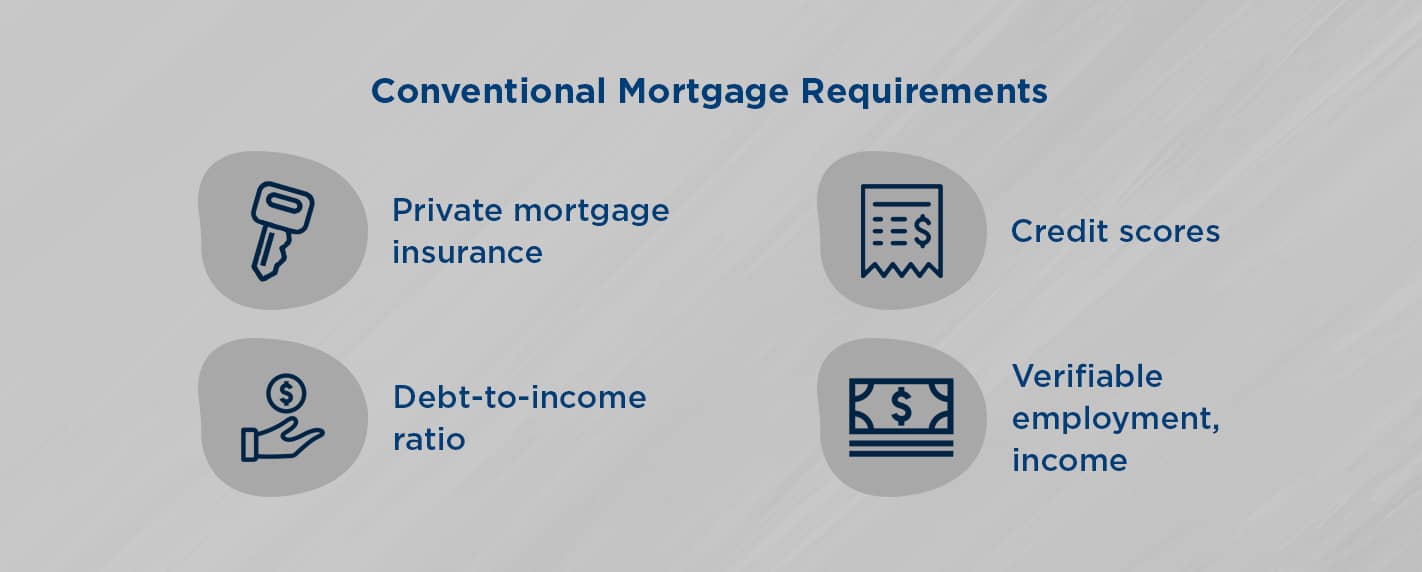

Lender's assessment of your information

To determine if you are a good risk, a mortgage lender will look at several factors. They'll examine your credit history, and look at any debt you have applied for. These details might be verified with your employer. They will also inspect your payment history. They will also check for any significant assets if they are available.

Lenders will want to see proof you are able to repay the loan. They may also be interested in your creditworthiness as well as your ability to pay off more debt. They use the five Cs of credit to determine creditworthiness: capacity, character, capital, collateral, conditions, and conditions.

Types and types of mortgages

There are several different types of mortgages. The first type is known as a conventional mortgage. A conventional mortgage can be used for most types of property. These loans are backed generally by the government and are easier to qualify for. These mortgages offer better rates for first-time homeowners and those with lower credit scores, higher debt-to–income ratios, and lower credit score.

The adjustable-rate mortgage (ARM) is the second type. People who want to adjust their interest rates can choose adjustable-rate mortgages. Another type of loan that is government-backed, such FHA, VA and USDA mortgages, is the FHA.

Refinancing options

There are many options available if you're looking to refinance your mortgage. You should shop around to find the best deal. The current interest rate is one of the biggest factors, so you should contact several lenders before deciding to refinance. You can also consult an attorney to assist you in the process.

Refinancing is a way to get the best out of your home's equity. Refinancing will lower your monthly cost and make it possible to achieve your financial goals. Refinance is a popular choice for people who want to reduce their monthly payments, get shorter terms and cash out their equity.

FAQ

Can I buy my house without a down payment

Yes! Yes. These programs include FHA, VA loans or USDA loans as well conventional mortgages. More information is available on our website.

How much money will I get for my home?

This can vary greatly depending on many factors like the condition of your house and how long it's been on the market. Zillow.com says that the average selling cost for a US house is $203,000 This

What are some of the disadvantages of a fixed mortgage rate?

Fixed-rate loans have higher initial fees than adjustable-rate ones. If you decide to sell your house before the term ends, the difference between the sale price of your home and the outstanding balance could result in a significant loss.

Do I need flood insurance?

Flood Insurance covers flooding-related damages. Flood insurance helps protect your belongings, and your mortgage payments. Find out more information on flood insurance.

Is it possible fast to sell your house?

It may be possible to quickly sell your house if you are moving out of your current home in the next few months. You should be aware of some things before you make this move. First, find a buyer for your house and then negotiate a contract. Second, you need to prepare your house for sale. Third, advertise your property. Finally, you should accept any offers made to your property.

Should I rent or buy a condominium?

Renting might be an option if your condo is only for a brief period. Renting lets you save on maintenance fees as well as other monthly fees. However, purchasing a condo grants you ownership rights to the unit. You are free to make use of the space as you wish.

How can I eliminate termites & other insects?

Over time, termites and other pests can take over your home. They can cause serious damage to wood structures like decks or furniture. To prevent this from happening, make sure to hire a professional pest control company to inspect your home regularly.

Statistics

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

External Links

How To

How to Find Houses to Rent

People who are looking to move to new areas will find it difficult to find houses to rent. Finding the perfect house can take time. When you are looking for a home, many factors will affect your decision-making process. These factors include size, amenities, price range, location and many others.

You should start looking at properties early to make sure that you get the best price. You should also consider asking friends, family members, landlords, real estate agents, and property managers for recommendations. This way, you'll have plenty of options to choose from.