A mortgage is a loan from a financial institution to a person or company. The lender expects that the borrower will repay the loan with interest. A person can also get a letter from a lender allowing them to borrow up to a certain amount. The lien may encroach upon the property's title and it can sometimes be difficult to clear. A mortgage with an adjustable rate can come with a life cap. This means that the rate for interest may not exceed a specified amount for a set period.

Amortization period

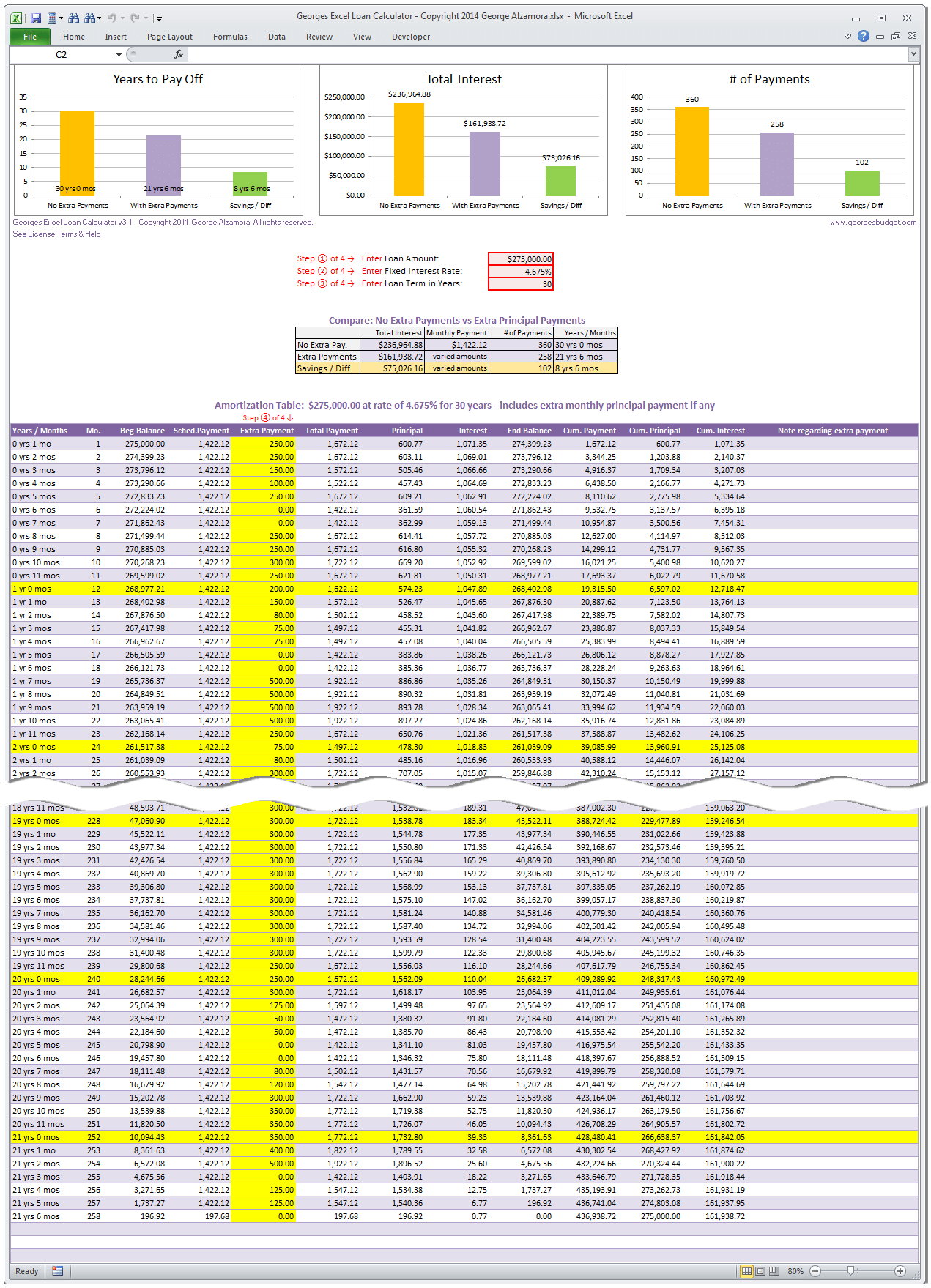

A mortgage refers to a loan that must paid back within a given time. This is known as the amortization term. The amortization time is typically represented by a table that indicates the percent of principal and/or interest that is paid in each payment. The total loan balance is also shown on the amortization schedule. The payments made in the early part of the term are typically principal and most are interest.

The amortization of a loan is one of the most important parameters in a mortgage contract. For first-time home buyers, a longer amortization time may be more advantageous as it will allow them pay off the loan quicker. If you prefer a shorter amortization period you might consider purchasing a home with a lower price.

Interest rate

The interest rate for a mortgage is what the lender charges you to borrow a loan. The interest rate is a percentage of principal amount. It is calculated each year. This rate will change depending on the terms. It will be lower for low-risk borrowers and higher for high-risk borrowers. Borrowers might also be familiar with the annual percentage return, or APY. This is the interest charged by banks to borrowers in addition to the principal amount.

Mortgage rates tend not to increase but your rate today might be lower than the rate in 2021, ten years or even a decade from now. Lenders don't keep mortgages for very long. Fannie Mae and Freddie Mac eventually sell them, and mortgage-backed securities are created from these mortgages. These mortgages are then sold to investors, who purchase them because they earn more than government notes.

Ratio loan-to value

It is important to take into account the loan-to value ratio (LTV) when searching for a mortgage. Your LTV should not exceed 80 percent. Any higher than that could lead to higher borrowing costs and even the denial of your loan. To avoid future problems, it's a good idea not to exceed 80%.

One way to reduce your LTV is to increase the amount of down payment. Negotiating a lower sales price can be done with your lender. Your interest rates will go down the lower you loan-to-value ratio.

FAQ

What are the key factors to consider when you invest in real estate?

The first thing to do is ensure you have enough money to invest in real estate. If you don’t have the money to invest in real estate, you can borrow money from a bank. Aside from making sure that you aren't in debt, it is also important to know that defaulting on a loan will result in you not being able to repay the amount you borrowed.

You must also be clear about how much you have to spend on your investment property each monthly. This amount must be sufficient to cover all expenses, including mortgage payments and insurance.

Finally, ensure the safety of your area before you buy an investment property. It would be best to look at properties while you are away.

Should I use a broker to help me with my mortgage?

Consider a mortgage broker if you want to get a better rate. Brokers have relationships with many lenders and can negotiate for your benefit. However, some brokers take a commission from the lenders. You should check out all the fees associated with a particular broker before signing up.

What are the benefits of a fixed-rate mortgage?

A fixed-rate mortgage locks in your interest rate for the term of the loan. This ensures that you don't have to worry if interest rates rise. Fixed-rate loans have lower monthly payments, because they are locked in for a specific term.

Is it possible fast to sell your house?

It might be possible to sell your house quickly, if your goal is to move out within the next few month. You should be aware of some things before you make this move. First, you will need to find a buyer. Second, you will need to negotiate a deal. You must prepare your home for sale. Third, your property must be advertised. Finally, you need to accept offers made to you.

Statistics

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

External Links

How To

How do you find an apartment?

The first step in moving to a new location is to find an apartment. This requires planning and research. It includes finding the right neighborhood, researching neighborhoods, reading reviews, and making phone calls. There are many ways to do this, but some are easier than others. Before renting an apartment, you should consider the following steps.

-

Data can be collected offline or online for research into neighborhoods. Online resources include websites such as Yelp, Zillow, Trulia, Realtor.com, etc. Local newspapers, landlords or friends of neighbors are some other offline sources.

-

You can read reviews about the neighborhood you'd like to live. Review sites like Yelp, TripAdvisor, and Amazon have detailed reviews of apartments and houses. You might also be able to read local newspaper articles or visit your local library.

-

You can make phone calls to obtain more information and speak to residents who have lived there. Ask them what they loved and disliked about the area. Ask if they have any suggestions for great places to live.

-

Take into account the rent prices in areas you are interested in. Consider renting somewhere that is less expensive if food is your main concern. On the other hand, if you plan on spending a lot of money on entertainment, consider living in a more expensive location.

-

Find out more information about the apartment building you want to live in. What size is it? How much is it worth? Is it pet-friendly? What amenities are there? Can you park near it or do you need to have parking? Do you have any special rules applicable to tenants?