A down payment will reduce the amount the lender has to lend you in order to purchase your home. For example, a 20% down payment will reduce the amount the lender must worry about if you stop paying. It is important to note that the down payment requirement is not set by the lender alone. It is also determined by the investor who is financing the loan.

For down payment, save

It is important to save for a downpayment on a mortgage in order to purchase a home. This process is similar running a marathon. While building up your savings, one dollar at a while, it is crucial to ensure that your finances are in order. You can do this by creating a budget, and directing funds to saving for a downpayment.

Re-selling items in your home is an excellent way to save money for a downpayment. This can be done through online marketplaces, local pawn shops and consignment stores. You can also sell your items at a yard sales to raise money for your downpayment. Include your partner's income.

Documentation is required

You will need the appropriate documentation in order to obtain a mortgage. The lender will need evidence of where your down payment funds came from. Even if you are sending a check from overseas, the lender will need to verify where the funds came from. Typically, lenders require a down payment to close the loan, although there are exceptions.

Most mortgage lenders will request your last two tax returns. Typically, they will require the most recent federal tax returns and state tax returns. You may also need additional income documentation.

Average down payment

The past year has seen record low mortgage rates, which has fueled a hot housing market. But what about an average downpayment? It will depend on the state you reside in. In early June 2021, the average down payment for a mortgage in California was over $100k, while the median down payment in a handful of other states was under $10k. Your equity will increase the larger your down payments, the lower your mortgage loan, and the smaller your down payment will be.

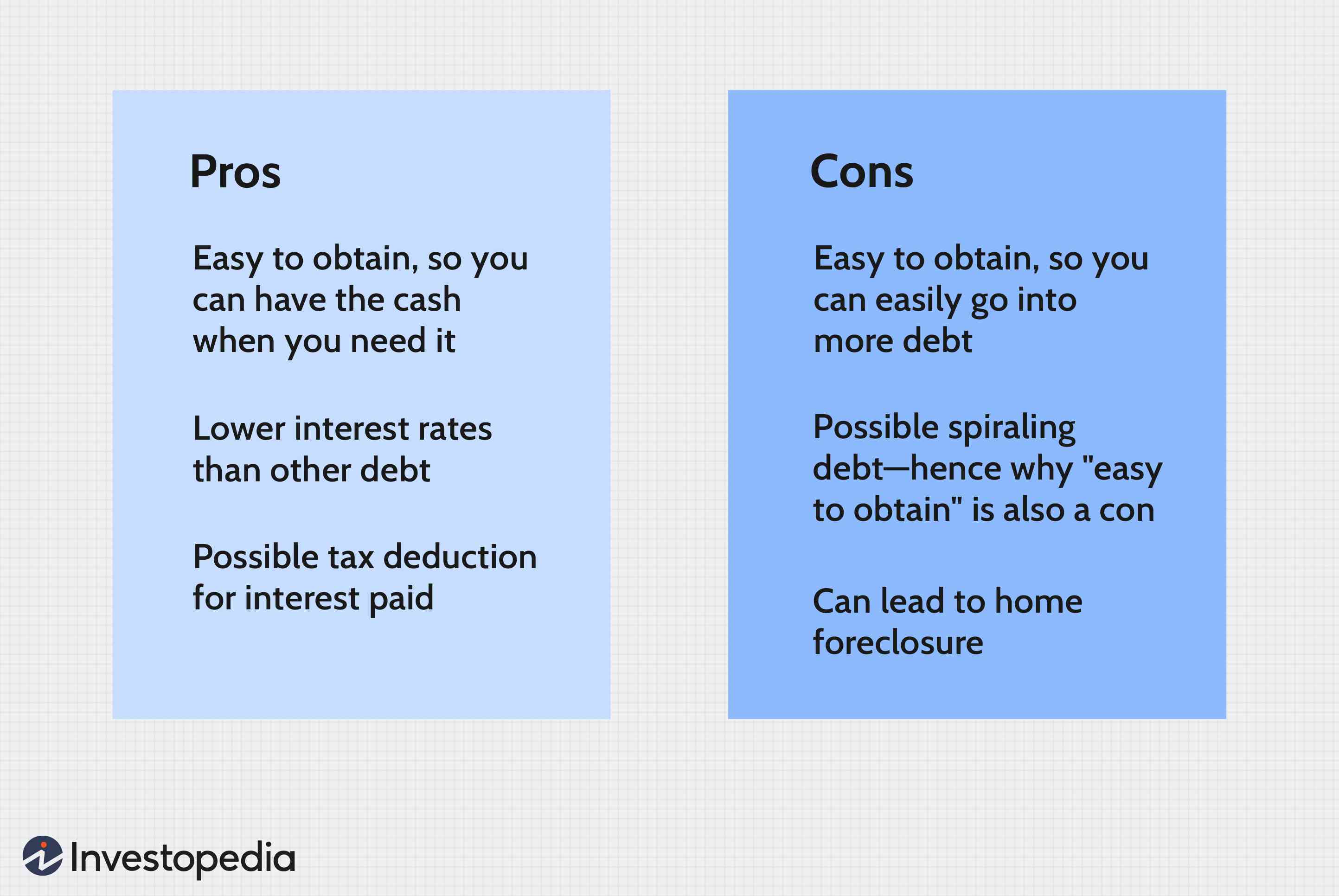

While some lenders require a 20 percent down payment, many people choose to put down a lower amount. A lower down payment will allow you to reach your goal faster. Consider the pros and cons before you decide on a downpayment amount.

Benefits from PMI

PMI will save your mortgage money, but there are some costs. The cost of PMI can run anywhere from 0.3 to 1.5 percent of the loan amount. This fee can be added to your monthly or final payment, or may be charged at closing. These fees vary depending on the mortgage you choose.

You can save on PMI by paying upfront. You will be able to lower your monthly payment but you may have to pay an annual fee that is not refundable if the move happens. Another option is to make partial payment each month and save money on your monthly premiums. This is particularly helpful if you have little down payments or need to save some cash.

The impact of a downpayment on the loan-to value ratio

The LTV (loan-to-value) ratio (LTV) will be affected by the down payment for mortgages. A larger down payment will translate into a lower LTV. This is because the lower the LTV ratio, the more equity you will have in your home. A small down payment can be increased to make your mortgage less expensive.

A loan with 80% LTV is available if your down payment exceeds 10% of the total cost. This will lower your chances of default and your monthly payments. Bankrate's mortgage calculator can help you figure how much you need to place down on your mortgage.

FAQ

How can I eliminate termites & other insects?

Your home will eventually be destroyed by termites or other pests. They can cause serious damage and destruction to wood structures, like furniture or decks. You can prevent this by hiring a professional pest control company that will inspect your home on a regular basis.

How many times may I refinance my home mortgage?

This will depend on whether you are refinancing through another lender or a mortgage broker. In either case, you can usually refinance once every five years.

Can I purchase a house with no down payment?

Yes! There are programs available that allow people who don't have large amounts of cash to purchase a home. These programs include FHA, VA loans or USDA loans as well conventional mortgages. Visit our website for more information.

What should you look for in an agent who is a mortgage lender?

A mortgage broker is someone who helps people who are not eligible for traditional loans. They look through different lenders to find the best deal. There are some brokers that charge a fee to provide this service. Others offer free services.

What's the time frame to get a loan approved?

It depends on many factors like credit score, income, type of loan, etc. It takes approximately 30 days to get a mortgage approved.

How can I determine if my home is worth it?

It could be that your home has been priced incorrectly if you ask for a low asking price. If you have an asking price well below market value, then there may not be enough interest in your home. To learn more about current market conditions, you can download our free Home Value Report.

Statistics

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

External Links

How To

How to buy a mobile house

Mobile homes are houses that are built on wheels and tow behind one or more vehicles. They were first used by soldiers after they lost their homes during World War II. People today also choose to live outside the city with mobile homes. These houses are available in many sizes. Some houses are small while others can hold multiple families. You can even find some that are just for pets!

There are two types of mobile homes. The first is made in factories, where workers build them one by one. This occurs before delivery to customers. You can also build your mobile home by yourself. Decide the size and features you require. Next, make sure you have all the necessary materials to build your home. The permits will be required to build your new house.

If you plan to purchase a mobile home, there are three things you should keep in mind. Because you won't always be able to access a garage, you might consider choosing a model with more space. A larger living space is a good option if you plan to move in to your home immediately. You should also inspect the trailer. If any part of the frame is damaged, it could cause problems later.

Before you decide to buy a mobile-home, it is important that you know what your budget is. It's important to compare prices among various manufacturers and models. Also, consider the condition the trailers. While many dealers offer financing options for their customers, the interest rates charged by lenders can vary widely depending on which lender they are.

Instead of purchasing a mobile home, you can rent one. Renting allows for you to test drive the model without having to commit. Renting is expensive. The average renter pays around $300 per monthly.